GST 2.0: Understanding India's New 3-Slab Tax Structure

Introduction

Is the newly introduced GST 2.0 truly simplifying India's tax regime or is it just rearranging old slabs under a fresh name?

Following the 56th GST Council meeting in September 2025, India implemented major reforms to its Goods and Services Tax, popularly dubbed GST 2.0. The overhaul is aimed at simplifying tax slabs, reducing compliance issues, and boosting consumption across the economy. These reforms took effect on 22 September 2025.

In this comprehensive analysis, we break down GST 2.0 and the new 3-slab structure, explain how it differs from the old system, highlight who benefits most, and offer practical guidance for businesses and consumers navigating these changes.

Understanding GST 2.0: What Has Changed

The 2025 reform represents the most significant restructuring of India's GST framework since its inception in 2017. The primary objective was to address long-standing concerns regarding the complexity of the previous multi-slab system, which often led to classification disputes, compliance burdens, and inverted duty structures.

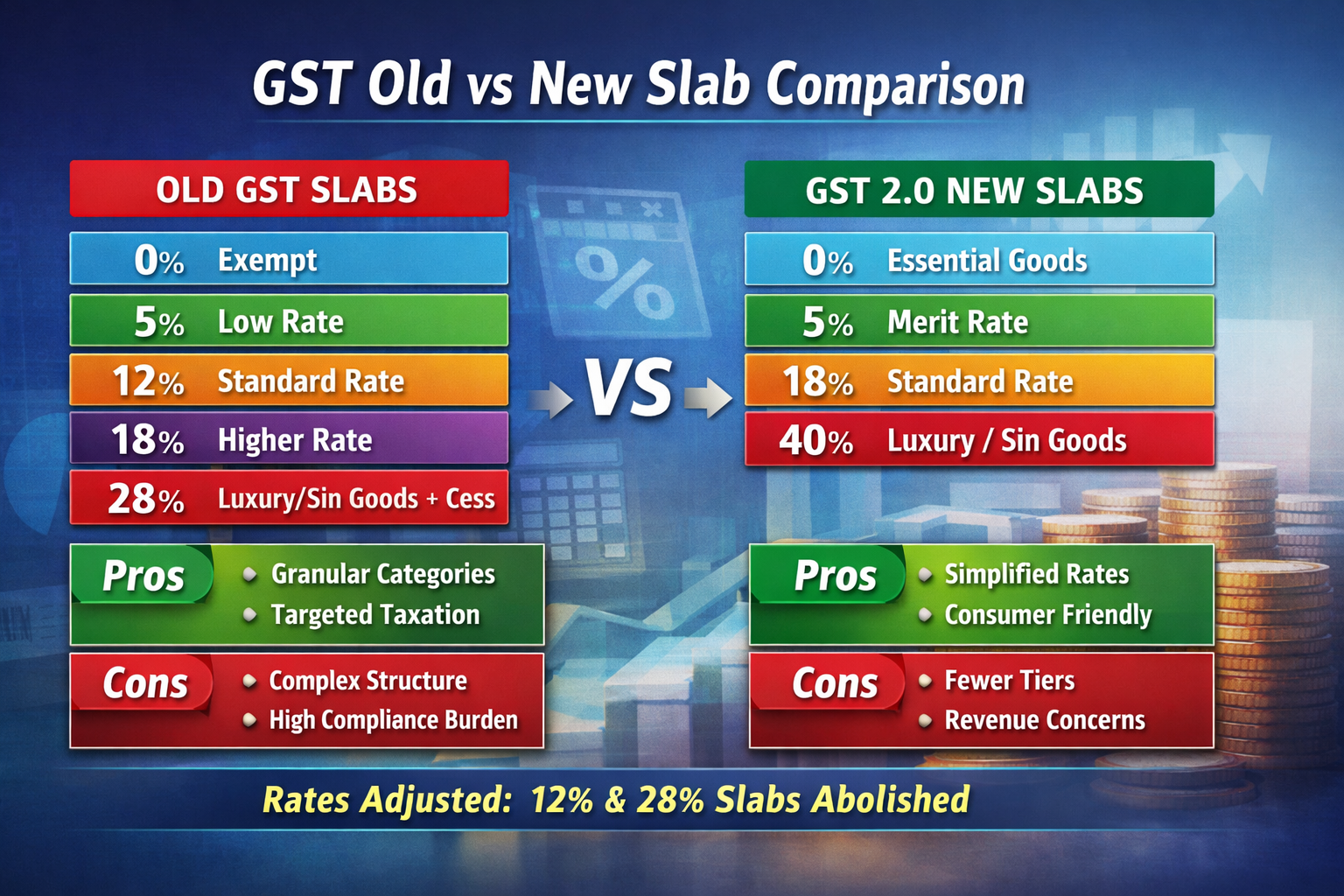

The New 3-Slab Structure

Under GST 2.0, the tax structure has been rationalised into a clearer framework:

| Slab | Description | Examples |

|---|---|---|

| 0% (Exempt) | Essential goods and basic services | UHT milk, paneer, stationery, life and health insurance |

| 5% (Merit Rate) | Daily essentials and mass-consumption items | Soaps, toothpaste, biscuits, dry fruits, basic FMCG goods |

| 18% (Standard Rate) | Majority of goods and services | Electronics, appliances, consumer durables, construction materials |

| 40% (Demerit/Luxury) | Luxury or harmful items | Tobacco products, pan masala, high-end vehicles, yachts |

Important Note: While technically a four-tier system when counting the 0% category, the 5%, 18%, and 40% rates are referenced as the main operational slabs in GST 2.0. The 12% and 28% slabs have been completely abolished.

Old vs New: How GST Slabs Have Shifted

Before the reforms, the GST regime in India had five main rates: 0%, 5%, 12%, 18%, and 28%, plus various special rates and a compensation cess on select items. This complexity often resulted in classification disputes and compliance challenges.

Key Structural Changes

- 12% and 28% slabs abolished: These intermediate rates have been eliminated entirely.

- Migration to 5%: Most goods previously in the 12% bracket now fall under 5%, making them cheaper for consumers.

- Migration to 18%: Many items in the 28% group are reclassified at 18%, lowering tax burden on mid-range goods.

- Introduction of 40% slab: A new higher rate for sin and luxury categories to maintain progressivity in taxation.

This rationalisation was designed to reduce tax complexity and ease classification disputes, a major cause of litigation under the older GST regime.

Comparative Analysis: Which Structure is Better?

Old Structure: Pros and Cons

| Aspect | Old GST Regime |

|---|---|

| Advantages |

|

| Disadvantages |

|

GST 2.0: Pros and Cons

| Aspect | GST 2.0 Regime |

|---|---|

| Advantages |

|

| Disadvantages |

|

Overall, GST 2.0 tilts toward simplicity and consumption-led growth, which many economists believe is better suited for India's large, diversified economy, particularly benefiting households and MSMEs.

Practical Examples: How This Affects Prices

Consumer Goods

- Everyday toiletries (soaps, toothpaste) taxed at 5% instead of 12-18%, reducing retail prices

- FMCG foods like biscuits, snacks, and coffee now attract lower GST

- Packaged foods including butter, cheese, and condensed milk moved to 5%

Electronics and Appliances

- Televisions, air conditioners, and refrigerators now at 18%, down from 28%

- Small cars (under 4 metres) attract 18% GST instead of higher previous rates

- Motorcycles under 350cc now taxed at 18%

Insurance Sector

- Life and health insurance premiums are fully exempt, giving direct relief to families and potentially expanding insurance penetration

Automobiles

- Small cars and two-wheelers attract 18% GST

- Luxury cars and high-end vehicles taxed at 40%

- Electric vehicles remain at 5%

Other Notable Changes

- Coal moved from 5% to 18%

- Aerated beverages with added sugar now at 40%

- Books and educational materials largely exempt

Guidance for Businesses

To navigate GST 2.0 effectively, businesses should take the following steps:

- Update accounting and billing software to reflect new slab mappings for all SKUs

- Re-train finance teams to understand revised rates and classification logic

- Reconcile past invoices and claim correct Input Tax Credit (ITC)

- Communicate price changes transparently to customers to manage expectations

- Monitor notifications from CBIC as further procedural changes roll out

Critical Action Item: Businesses must ensure their GST returns reflect the new rates from 22 September 2025 onwards. Failure to update systems could result in incorrect tax collection and compliance issues.

Revenue Impact and Fiscal Considerations

The government has estimated a net revenue implication of approximately Rs. 48,000 crore from these reforms. However, several factors may offset this:

- The 40% sin/luxury slab is expected to recoup revenue from inelastic categories

- Improved compliance and reduced leakages may partially offset losses

- Higher economic growth and expanded tax base could improve revenue buoyancy

- The effective weighted average GST rate may fall to approximately 9.5%

Conclusion: GST 2.0 and the Path Forward

GST 2.0 represents the most significant rework of India's GST regime since its inception in 2017, aiming for simplicity, broader compliance, and enhanced consumer benefits. By collapsing multiple slabs into a streamlined structure, the government has addressed long-standing concerns about complexity while maintaining progressivity through the 40% demerit rate.

While debates will continue about optimal slab structures, the current framework balances ease of doing business with fiscal pragmatism. Whether you are a business owner, tax professional, or everyday consumer, understanding these changes is crucial to realising the full benefits and staying compliant under the new GST 2.0 system.

At AAG & Co., we specialise in GST compliance and advisory services to help businesses navigate these transitions seamlessly. Contact our team for personalised guidance on optimising your tax strategy under GST 2.0.

CA Archit Agrawal

Specialised in GST compliance, indirect taxation, and regulatory advisory. Our team of Chartered Accountants and tax professionals helps businesses navigate complex tax landscapes with precision and strategic insight.