Understanding the GST Invoice Management System (IMS): A Comprehensive Guide for 2026

Introduction

What if a single change on the GST portal could transform how your business claims Input Tax Credit (ITC)? This is not just a hypothetical scenario. The Invoice Management System (IMS) introduced on the GST portal is fundamentally reshaping the way taxpayers reconcile invoices, correct discrepancies, and ensure accurate tax compliance.

Effective from 1 October 2024, the IMS represents a significant shift from passive invoice viewing to active invoice management. This comprehensive guide explores everything you need to know about the IMS, how it compares with the previous system, and why it matters for your business in 2026.

What Is the Invoice Management System (IMS)?

The Invoice Management System (IMS) is a digital dashboard introduced by the Goods and Services Tax Network (GSTN) that empowers recipient taxpayers to directly manage inward supply invoices uploaded by their suppliers. Unlike the previous passive viewing system, IMS enables active decision-making on every invoice before it impacts your tax credits.

Key Functional Capabilities

- Automated Invoice Flow: Supplier invoices from GSTR-1, GSTR-1A, and IFF automatically populate the recipient's IMS dashboard in real-time

- Actionable Controls: Recipients can accept, reject, or mark invoices as pending before they reflect in GSTR-2B

- Deemed Acceptance Protocol: If no action is taken by the due date, invoices are automatically deemed accepted and included in GSTR-2B for ITC purposes

- Amendment Tracking: Suppliers can view recipient actions and amend rejected invoices for re-upload

Critical Insight: The IMS transforms invoice reconciliation from a post-filing correction exercise to a pre-filing validation process, significantly reducing compliance risks and ITC mismatches.

Why Was the IMS Introduced?

Previously, mismatches between supplier-reported invoices and ITC claimed by recipients were a persistent compliance challenge. Taxpayers often discovered errors only when filing returns, leading to notices, interest liabilities, and complex adjustment procedures.

Strategic Objectives

- Enhance ITC Accuracy: Enable real-time invoice validation and reconciliation before credit claims are finalized

- Mitigate Compliance Risks: Facilitate direct communication between suppliers and recipients to resolve discrepancies proactively

- Streamline Audit Processes: Maintain comprehensive records of invoice actions (accept/reject/pending) for transparency

- Prevent Fake Invoice Fraud: Strengthen controls against ineligible ITC claims by requiring recipient verification

How the IMS Works: Step-by-Step Process

Understanding the workflow is essential for maximizing the benefits of IMS. The process creates a collaborative ecosystem between suppliers and recipients.

| Step | Action By | Process Details |

|---|---|---|

| 1. Invoice Upload | Supplier | Supplier files invoices in GSTR-1, GSTR-1A, or IFF |

| 2. Dashboard Population | System | Invoices automatically appear in recipient's IMS dashboard |

| 3. Recipient Action | Recipient | Review and select Accept (A), Reject (R), or Pending (P) |

| 4. Supplier Notification | System | Rejected invoices notify suppliers for correction |

| 5. GSTR-2B Generation | System | Draft GSTR-2B generated on 14th of subsequent month |

| 6. Final ITC Computation | System | Only accepted/deemed accepted invoices flow to GSTR-3B |

Action Definitions

- Accept (A): Invoice is approved and included in GSTR-2B under "ITC Available" section. GST amount auto-populates in GSTR-3B as eligible ITC.

- Reject (R): Invoice is excluded from ITC computation. Moved to "ITC Rejected" section of GSTR-2B. Does not auto-populate in GSTR-3B.

- Pending (P): Invoice is set aside for future action. Not included in current period GSTR-2B or GSTR-3B. Remains in IMS dashboard for subsequent period action.

Important: Pending action is not permitted for original credit notes, upward amendments of credit notes, or downward amendments where original invoices were already accepted and GSTR-3B filed.

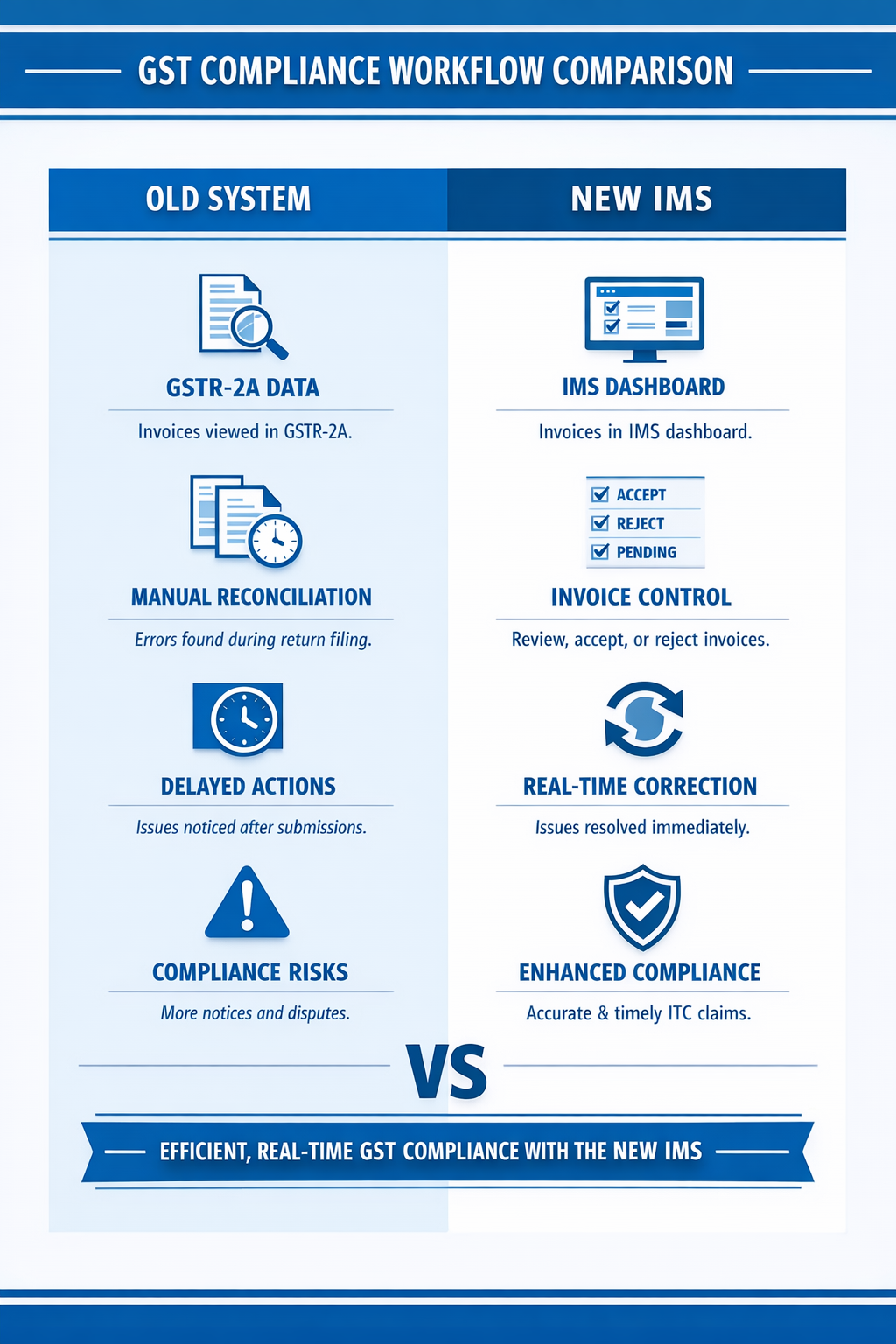

IMS vs. Previous System: Comparative Analysis

The shift from the traditional GSTR-2A/2B viewing system to IMS represents a paradigm change in GST compliance methodology.

| Parameter | Pre-IMS System | With IMS Implementation |

|---|---|---|

| Invoice Visibility | Visible only after supplier files GSTR-1 | Visible immediately when supplier saves in GSTR-1/IFF/1A |

| ITC Claim Process | All invoices in GSTR-2B considered for ITC; disputes reversed later | Only accepted invoices appear in GSTR-2B; disputes rejected upfront |

| Reconciliation Timing | Post GSTR-2B generation; last-minute adjustments in GSTR-3B | Real-time reconciliation before GSTR-2B generation |

| Amendment Handling | Amendments reflected in next month's GSTR-2B | Amendments visible immediately in IMS for quicker correction |

| Credit Note Control | Automatically considered in GSTR-2B without recipient acknowledgment | Can be rejected in IMS; recipient controls ITC reversals |

| Supplier Communication | Limited offline communication; mismatches discovered late | Enhanced portal-based communication at invoice level |

| Default Treatment | All supplier-reported invoices auto-included in GSTR-2B | No-action invoices deemed accepted; rejected invoices excluded |

Latest Enhancements in IMS (Post-2024)

The GSTN has continuously refined the IMS based on taxpayer feedback and evolving compliance requirements. Key upgrades effective from October 2025 include:

Pending Credit Notes Functionality

From October 2025, credit notes and certain records can be marked as pending for one tax period. This provides flexibility in handling complex credit scenarios without immediate ITC impact.

Enhanced ITC Reversal Options

Taxpayers now have granular control with the ability to declare full or partial reversal amounts. This precision in ITC adjustments accommodates complex business scenarios where complete reversal is not required.

Transparency Through Remarks

The system now allows users to save remarks when rejecting or marking invoices as pending. This audit trail enhances transparency between business partners and provides documentation during scrutiny proceedings.

Compliance Note: These enhancements reflect the GST Council's commitment to reducing compliance burden while maintaining robust audit trails. Businesses should update their standard operating procedures to leverage these new capabilities.

Practical Implementation: Case Study

Consider Company A, a manufacturing entity, which receives an invoice of Rs. 2,00,000 from Supplier B. Upon review, the accounts team notices a discrepancy in the GST amount reported.

Scenario Without IMS (Legacy Process)

- Error detected only during GSTR-3B filing or audit

- ITC claimed incorrectly, requiring reversal with interest

- Communication with supplier through offline channels

- Potential compliance notice for mismatched claims

- Amendment reflected only in subsequent month returns

Scenario With IMS (Current Process)

- Company A rejects the invoice immediately in IMS dashboard with remarks

- Supplier B receives real-time notification of rejection

- Supplier B corrects and re-files the invoice before return deadline

- Company A accepts the corrected invoice for ITC

- Accurate ITC claimed without compliance hassles or reversals

Result: Zero compliance risk, accurate ITC claim, and strengthened supplier relationships through transparent communication.

Strategic Recommendations for IMS Optimization

To maximize the benefits of IMS and ensure seamless compliance, businesses should implement the following practices:

1. Establish Regular Monitoring Protocols

Designate specific team members to review the IMS dashboard daily. This prevents default "deemed acceptance" of erroneous invoices and ensures proactive management of inward supplies.

2. Implement Supplier Communication Frameworks

Develop standard operating procedures for communicating rejections to suppliers. Clear, documented communication reduces resolution time and prevents recurring errors.

3. Strategic Use of Pending Status

Utilize the pending action strategically when awaiting clarifications or documentation. This prevents immediate ITC impact while preserving the option to accept later, subject to Section 16(4) time limits.

4. Maintain Comprehensive Audit Trails

Leverage the remarks functionality to document reasons for rejections or pending actions. These records prove invaluable during departmental audits and assessments.

5. Integration with Internal ERP Systems

Where possible, integrate IMS data with internal accounting systems to automate reconciliation processes and reduce manual data entry errors.

Conclusion

The Invoice Management System represents more than a technological upgrade; it is a strategic compliance tool that fundamentally transforms how businesses manage their GST obligations. By shifting from passive invoice viewing to active invoice management, the IMS empowers taxpayers to control, verify, and manage their GST invoices with unprecedented precision.

The system's ability to facilitate proactive actions on supplier invoices, combined with tools for precise ITC management, enhances transparency, reduces disputes, and strengthens overall GST compliance. Whether operating as a small business or a large enterprise, understanding and leveraging the IMS is now essential for minimizing compliance risks and maximizing accurate tax credits.

As the GST ecosystem continues to evolve, early adoption and mastery of IMS workflows will provide competitive advantages through improved cash flow management and reduced compliance costs. At AAG & Co., we recommend immediate implementation of IMS review protocols to ensure your business remains compliant and optimized in the current tax landscape.

Anuj Kumar Mittal

Chartered Accountant specializing in GST compliance, direct taxation, and corporate advisory. Our team provides expert guidance on navigating complex tax regulations and optimizing compliance frameworks for businesses across India.